Executive Summary

In Q1 2025, the tech M&A landscape was shaped by a sharpened focus on AI infrastructure, financial discipline, and dealmaking creativity amid continued macroeconomic uncertainty. AI-related transactions surged, accounting for an estimated $60 billion in deal value as acquirers prioritized strategic capabilities in areas like edge computing, robotics, and quantum tech. Private equity firms quietly dominated activity, leveraging record dry powder to execute carve-outs and take-private deals, especially in Europe. Facing tight financing conditions, buyers leaned on structured deal terms—earnouts, deferred payments, and mergers of equals—to bridge valuation gaps and mitigate risk. Diligence efforts increasingly centered on revenue retention, operational efficiency, and AI compliance, driven by emerging global regulation. With M&A values rising 15% despite fewer deals, the outlook remains strong but selective, with a continued emphasis on capital-efficient, high-retention software platforms and defensible growth in AI, fintech, and sustainability.

The New Arms Race – Acquirers are stockpiling AI infrastructure

The competitive drive toward AI readiness intensified significantly: AI and data infrastructure transactions captured an estimated 25% of tech-related M&A deal value in Q1, amounting to over $60 billion globally. Dealmakers remained highly selective, zeroing in on companies with proven IP and niche capabilities in areas like robotics, hyperscale data centers, and agentic AI platforms. Examples include UiPath or edge-AI solutions that can run critical analytics on-device. Key highlights include:

- Qualcomm’s strategic $2.4 billion acquisition of Alphawave, bolstering its semiconductor and interconnect portfolio essential for advanced AI workloads.

- IonQ’s $1.1 billion takeover of Oxford Ionics, signaling a surge of interest in quantum computing as a long-term accelerator for AI and materials science.

- Meta’s $14.8 billion investment in Scale AI, deepening its data labeling and AI services capabilities in preparation for broader monetization of its metaverse and advertising platforms.

The PE Playbook Reloaded – Buyout firms quietly dominating Q1 tech M&A

Private equity firms ramped up activity in Q1, with deal volumes rising 45% year-over-year. Armed with record-high dry powder—exceeding $2 trillion globally—PE players like Blackstone, Carlyle, and KKR targeted undervalued and cash-flow-positive tech assets, especially in Europe. Their playbooks leaned heavily on take-private transactions, operational turnarounds, and margin expansion initiatives. In many cases, PE-backed carve-outs and bolt-on acquisitions are consolidating fragmented verticals in software and services, driving scale and efficiency.

The Age of Discipline – M&A adapts to caution and creativity

With interest rates elevated and financing conditions tighter, dealmakers increasingly turned to creative structures to bridge value and risk gaps:

Structured Consideration: Earnouts, deferred payments, equity rollovers, and even revenue-sharing mechanisms became standard in mid-market tech deals, helping buyers and founders align incentives and manage near-term performance uncertainty.

Private Reverse Mergers (PReMs) & SPAC 4.0: A modest SPAC revival saw Goldman Sachs roll out “SPAC 4.0,” featuring lighter capital raises (~$200 million), enhanced governance, and refined risk controls. Blue Ant Media’s reverse merger of Boat Rocker in March 2025 exemplified the renewed but cautious SPAC appetite.

Mergers of Equals (MoEs): The Printify–Printful merger illustrated how two scale-ups can combine complementary e‑commerce printing platforms to achieve rapid scaling, $100 million+ in projected cost synergies, and cross-selling opportunities across 150 markets.

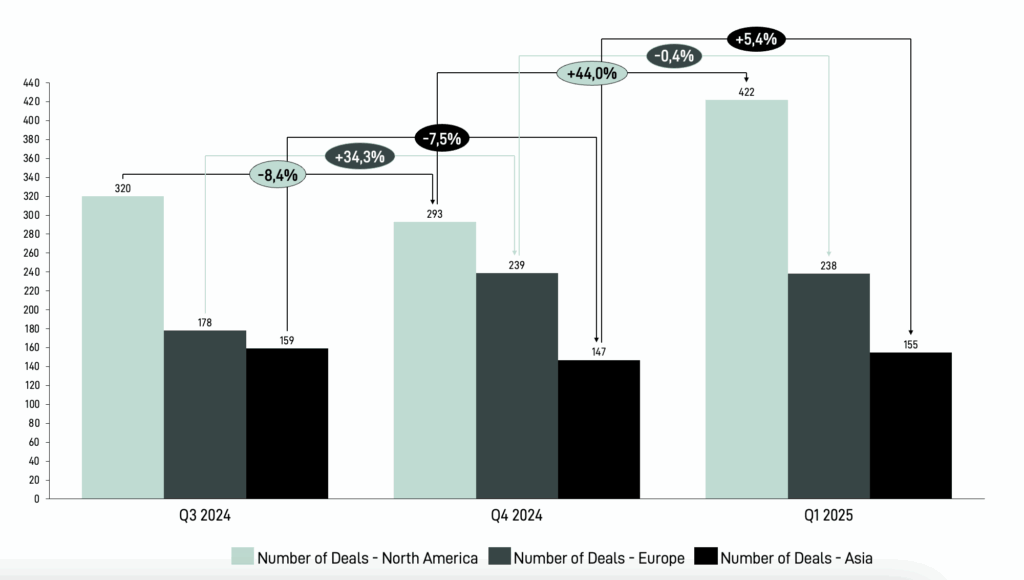

Tech M&A Activity Snapshot

Source: Preqin June 2025

Throughout Q1, dealmakers faced high borrowing costs, tariff uncertainties, and a shifting regulatory backdrop. In response, they focused on mid-market targets with visible recurring revenues—particularly vertical SaaS, infrastructure software, and AI-native platforms offering strong retention, embedded analytics, and predictable cash flows.

Regulators signaled a pragmatic turn on large tech transactions: Google’s previously shelved $32 billion acquisition of Wiz was revived under lighter antitrust scrutiny, encouraging confidence in cross-border and large-scale transactions. Meanwhile, structured deal terms—like sandbagging clauses and collar protections—became table stakes, ensuring both parties could share in upside while mitigating downside risk.

Key Challenges and Diligence Focus

Capital with Conditions

Although debt markets remain open, roughly 35% of M&A practitioners expect financing to tighten further over the next two quarters. Private credit funds are bridging some gaps, but lenders demand detailed operational projections, coverage ratio covenants, and robust stress tests.

Revenue Only as Good as Retention

Buyers increasingly prioritize the sustainability and predictability of recurring revenues. Net revenue retention (NRR) benchmarks above 110–120%, gross churn rates under 5%, and robust customer lifetime value (LTV) metrics are now standard expectations. Comprehensive cohort analysis and predictive retention modeling are critical to accurately assess revenue quality and future growth potential.

Efficiency As the Exit Strategy

Given a tighter financing environment, companies must clearly demonstrate operational efficiency and robust unit economics. The Rule of 40 (combined revenue growth and EBITDA margin exceeding 40%) remains a pivotal metric in diligence of tech companies. Investors closely examine CAC payback periods, Burn Multiples, and clear pathways to profitability, making detailed financial modeling and rigorous scenario planning essential.

AI Under Review

In Q1 2025, the EU’s AI Act moved closer to implementation, with draft enforcement timelines released. This prompted buyers to intensify due diligence on AI-related acquisitions—particularly those involving generative AI and machine learning. Focus areas included data provenance, model transparency, and compliance with training data regulations. Simultaneously, regulators in the US, UK, and Canada signaled growing alignment with the EU’s approach, suggesting the emergence of a more globally coordinated AI oversight landscape. As a result, buyers expanded their diligence scope to cover consent mechanisms and AI system governance—areas that had historically received less attention in traditional M&A processes.

Outlook for the Rest of 2025

Still Strong, But Sharper

The strong momentum seen in Q1 2025—where global M&A values rose 15% to $1.5 trillion despite a 9% drop in deal volumes—is expected to continue into the second half of the year. Early Q2 activity points to a sustained focus on high-value, high-conviction deals, especially in the tech sector, which recorded $64 billion in Q1 alone—its highest quarterly total since early 2024. Strategic buyers and private equity firms remain focused on AI infrastructure, cloud platforms, and hyperscale data assets, while defense and climate tech are emerging as key growth areas.

Mid-Market, Maximum Efficiency

Mid-market M&A is also expected to remain active as acquirers prioritize capital-efficient software companies with durable economics. Buyer interest is especially high in three areas:

- AI platforms – including edge analytics and quantum-enabling capabilities that drive enterprise automation and resilience;

- ESG and sustainability software – such as carbon accounting and compliance tools, fueled by rising regulatory demands;

- Vertical fintech platforms – serving logistics, payments, and B2B workflows, benefiting from ~21% YoY revenue growth and improved margin profiles.

These businesses offer sticky revenue, high retention, and clear paths to scale—qualities that increasingly define attractiveness in a capital-conscious market.

Selectivity Is the New Scale

Looking ahead, dealmaking is expected to remain steady but selective. Buyers will likely concentrate on fewer, more strategic acquisitions that offer both defensible growth and operational transparency. Structured terms—such as earnouts, deferred payments, and equity rollovers—will remain essential tools for bridging valuation gaps in a cautious financing environment. Companies that invest early in operational readiness, scenario planning, and regulatory alignment will be best positioned to capture value in a more disciplined and data-driven market.

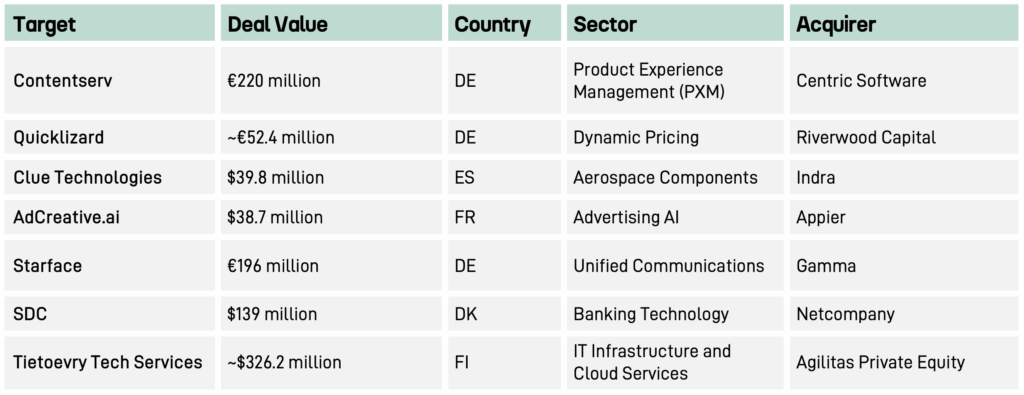

Notable Q1 European AI Acquisitions

Did you know that we started publishing on Medium? Make sure to check it out here.