Earnouts are an integral component of M&A deal terms, as they help sellers and buyers to align their expectations on valuations. Drawing from our experience at Samira Advisors, there are various focal areas that need to be thought about before entering earnout negotiations.

Earnouts as a tool to bridge valuation gaps

Selling a business involves navigating a complex journey, with a key focus on determining its value. Differing perspectives can lead to intense negotiations between sellers and buyers, as each party seeks a purchase price that reflects their personal assessment of the company’s value. To bridge the gap between the seller’s ask and the buyer’s willingness to pay, earnouts established themselves as an attractive strategic tool to reconcile company valuations. An earnout is an extra future payment tied to the company’s performance after the acquisition. It is tied to mutually agreed-upon metrics that monitor the post-deal performance. These metrics can be financial (e.g., revenue or EBITDA) or non-financial (e.g., user growth or retention rates). Earnouts usually last 2–3 years post-closing and include milestones that can be reached prior to the final deadline.

Success factors and relevant considerations for founders

Earnouts aim to align expectations and promote future value creation while avoiding misunderstandings. Well-structured earnouts benefit both seller and buyer, fostering a “grow the pie” outcome. For instance, they may elevate the business valuation for the seller and reduce upfront costs for the buyer.

To secure mutual value from earnouts, founders must navigate two potential pitfalls. Firstly, earnouts carry a vital signaling effect during negotiations. They are often based on pre-acquisition forecasts. Reluctance to tie them to those might signal a lack of confidence in the projected performance, ultimately granting the buyer negotiation leverage and influencing deal terms. Secondly, the achievement of earnouts will depend on the company’s new strategic direction under new post-acquisition ownership. Founders must assess whether this aligns with their vision for the company’s future and if it is the right path forward.

Although earnouts can effectively “grow the pie” for both sellers and buyers, investors of the selling company often view earnout provisions with caution. Their concern arises from the passive role they play in an earnout scenario, often leaving them in the middle ground of the transaction. Their final payout, in fact, also depends on the achievement of the earnout targets, and this depends on variables beyond their control.

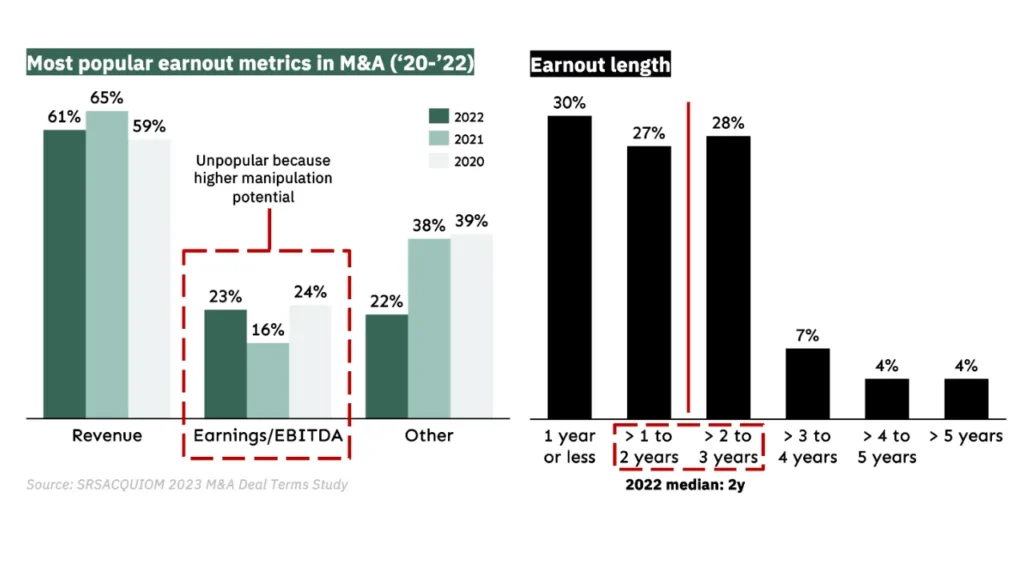

While revenue and EBITDA might seem inherently clearly defined, it’s essential to consider challenges when tying earnouts to these metrics. For instance, revenue can be defined as total or operating revenue, impacting future earnout target achievement. Vague definitions may lead to disputes. Similarly, EBITDA can be influenced by the acquirer by charging various intercompany expenses. As depicted in the chart above, this vulnerability leads to its lesser popularity in earnout structuring. These examples underscore the importance of defining earnout measurement metrics clearly and in a business-savvy manner, minimizing the likelihood of disputes and establishing concrete expectations for future payouts.

Case Study: Navigating a Purchase Price Deadlock with Earnout

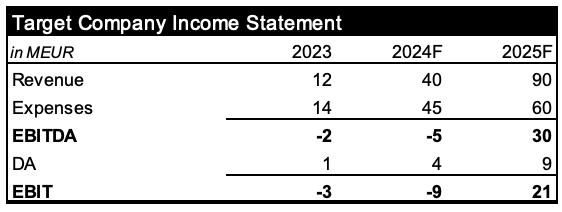

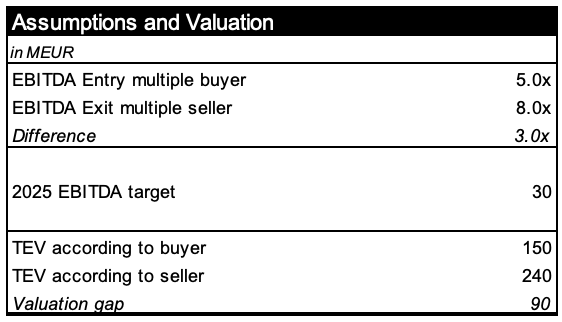

The shareholders of a digital platform startup are in the final negotiation round with a larger strategic acquirer. The Target’s forecasted income statement indicates a temporary loss before a crucial inflection point in 2025, where profitability is anticipated.

Based on the provided forecast, the seller and the buyer independently conducted valuations. For simplicity, both parties assumed the company’s purchase price using a total enterprise value-based multiple (TEV/EBITDA). Given the Target’s current negative EBITDA, they agreed to value the company based on a projected positive EBITDA target in 2025. The table below outlines the valuation assumptions and the corresponding total enterprise values assigned to the Target. It is clear that the individual valuations resulted in a substantial gap of €90M, primarily due to the differing multiples used in the calculations.

Both the seller and the buyer are still convinced their assumptions and valuations are correct. Despite being stuck in a purchase price deadlock, both parties still commit to closing the transaction and opt for an earnout to reconcile the valuation gap.

Based on our experience, the following procedure guides us through an earnout structuring process:

- Set the ceiling: The negotiation begins by determining the highest amount the seller could eventually receive. Both seller and buyer agree on 70% of the seller’s ask, resulting in a potential €168M payout. This step is intended to bridge the initial valuation gap partially.

- Lay the floor: In most cases, it is constituted by the buyer’s proposed total enterprise value (TEV). Using the example, the upfront payment would be the initially offered €150M. The combined effects of the first and second steps have already reduced the valuation gap from €90M to a mere €18M.

- Adjust the timeline: Seller and buyer agree on a two-year earnout period spanning 2024 and 2025 to bridge the remaining €18M valuation gap. This reflects the median duration of an earnout period.

- Hang the bull’s eye: In this case, the parties agree on a singular metric, the absolute level of EBITDA achieved by 2025, as this was used as a base for both valuations. The pool of performance measurement metrics could be extended with further financial and non-financial metrics such as user retention, user growth, and user retention.

- Craft the payment blueprint: The final step involves the parties agreeing on the payment schedule. Are the earnouts divided into several measurement and payout periods, or does the end result solely determine the amount paid out?

Summing up, earnouts are a tool to bridge valuation gaps in M&A transactions that aim to benefit both the seller and the buyer. Nevertheless, there are specific pitfalls that founders need to be aware of when entering earnout negotiations. Examples are signaling effects as well as the possibility of new shareholders pivoting the company to a strategic direction that doesn’t align with the founder’s vision. Lastly, it is essential to structure the earnout process efficiently in order to reap the maximum benefits for both parties.