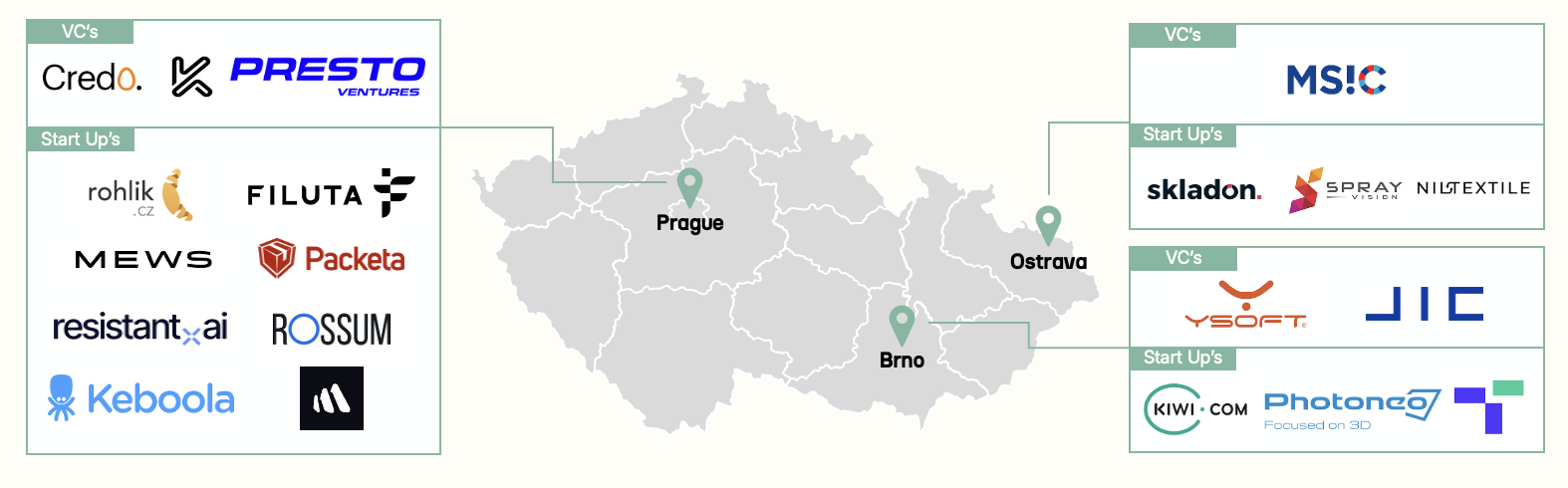

3. Start-up hubs in the Czech Republic

3.1 Three major hubs, with Prague on top

The Czech tech landscape is anchored by three power centers, each playing a distinct strategic role in the ecosystem:

Prague: Prague serves as the undisputed “ecosystem headquarters.” This is where capital and scaling expertise concentrate, particularly in Fintech, SaaS, and Corporate Innovation. With accelerators like Start it @ČSOB and innovation hubs such as Škoda X, the city is the primary destination for founders seeking proximity to investors, regulators, and large B2B buyers.

Brno: The region is widely regarded as the most “organized” ecosystem in the country. Driven by the JIC (South Moravian Innovation Centre), Brno has established itself as a stronghold for Cybersecurity, IoT, and semiconductor technology. Through tight links with top-tier research centers like CEITEC, the region produces technologically complex solutions that often achieve global niche leadership.

Ostrava: Ostrava leverages its industrial DNA to lead in digital transformation. The centerpiece is the IT4Innovations National Supercomputing Center, which anchors the “Czech AI Factory” project. By hosting the AI-optimized supercomputer “KarolAIna,” the region provides the actual compute power and infrastructure necessary for high-scale AI startups and applied industrial research.

4. Funding: Plenty early, thinner later

4.1 Where the money actually went

Even though Czechia’s local ecosystem is structurally strongest at pre-seed/seed, recent funding data shows that meaningful capital does get deployed into Czech-founded companies — often with international investors or cross-border syndicates involved.

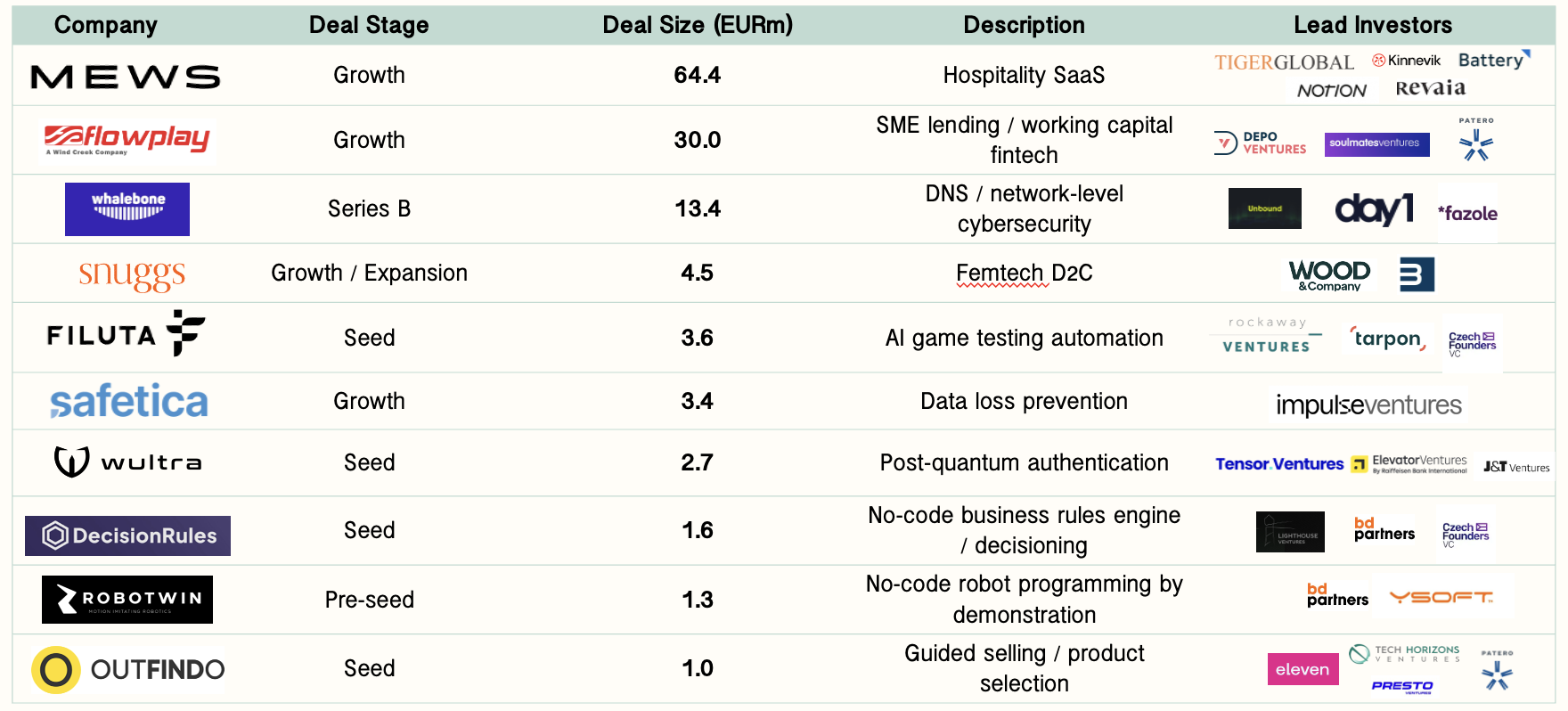

Top rounds in 2025 (selected)

Based on H1 2025 deal evidence, Czechia’s funding highlights a skew toward pragmatic, exportable B2B products rather than purely local-market consumer plays. A notable cluster appears in cybersecurity (e.g., Whalebone, Safetica, Wultra), alongside vertical/enterprise software and infrastructure themes (Mews in hospitality operations, DecisionRules in business rule automation, Flowpay in SME financing). At the upper end, the largest rounds tend to be internationally syndicated, reinforcing the pattern that late-stage capital is available but often requires cross-border investor access and narrative positioning.

4.2 Key dynamics

The Czech tech economy exhibits a top-heavy structure where massive value concentration in Prague sits alongside significant structural hurdles. The capital remains the undisputed engine of growth, with an ecosystem value of €19.2 billion, representing roughly 83% of the national total. This concentration is especially visible in the AI sector, which now secures nearly one-third of all venture capital funding in the country.

Despite this success, 2026 data highlights deep-seated friction points. Approximately 72% of founders cite the tax burden as a primary barrier, while 64% point to excessive bureaucracy. These challenges have led a third of startups to consider or complete a move of their headquarters abroad. Furthermore, the era of the “cheap engineer” has ended; average ICT salaries reached 94,000 CZK in 2024, and senior roles in Prague now frequently exceed 125,000 CZK, driven by high demand and rising government salary thresholds for foreign talent.

Finally, the investor landscape faces a “selectivity bottleneck.” While top-tier companies thrive, 62% of local investors report a lack of high-quality, investment-ready startups. This has created a stark divide, where elite assets price globally and attract international interest, while median startups face a much tougher and more cautious fundraising environment.

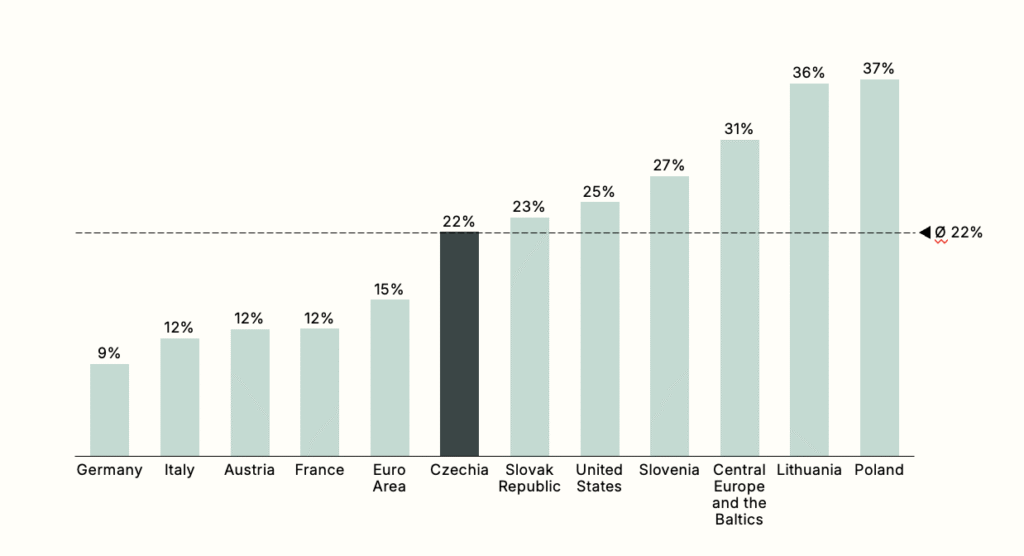

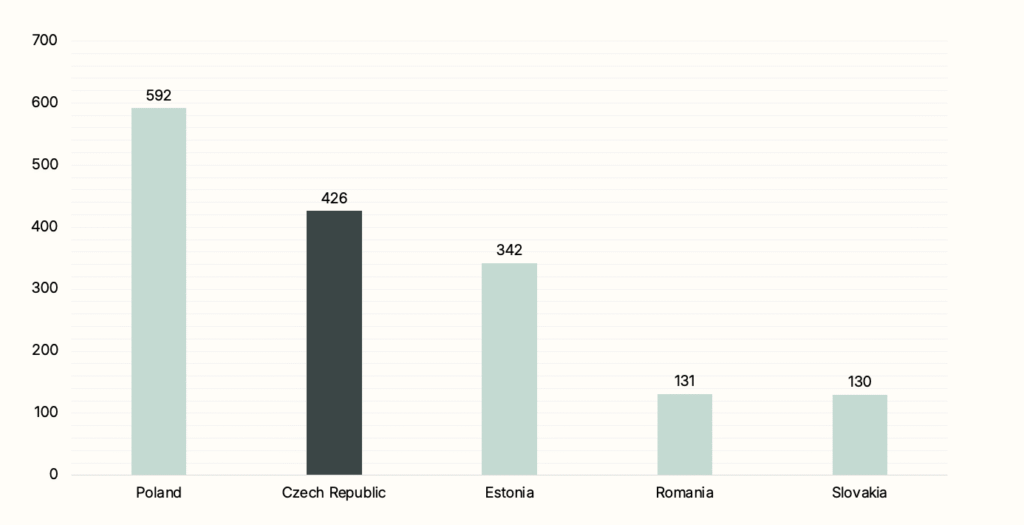

This competitive landscape is best understood within the broader regional context of Central and Eastern Europe. While Czechia faces internal pressures, it remains a dominant force in the region, often vying for the top spot in total investment value. The following table illustrates how Czechia’s funding volume and ecosystem maturity compare to its neighbors.

VC funding Comparison – Eastern Europe (in EURm)

5. M&A: Buyers come from outside

5.1 The Exit Strategy: Trade Sales as the Default Path

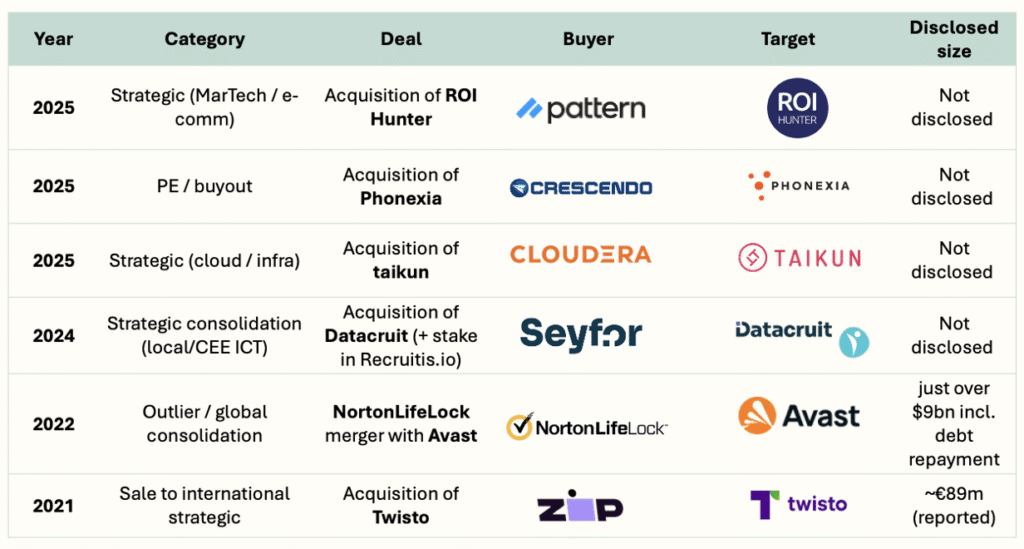

For the vast majority of Czech tech companies, trade sales to strategic buyers remain the primary exit route. While “mega-deals” like the $9B Avast-NortonLifeLock merger prove that Prague can produce global giants, most successful outcomes are mid-market cross-border acquisitions. In 2024, the broader Czech M&A market recorded approximately 128 deals with a total value of €5.65B, with software and IT services consistently ranking as the most active sub-sectors.

For founders, exits typically fall into three distinct categories. Cross-border M&A is the standard “VC-style” win, where international strategics acquire Czech startups for their technical talent and European market access. A classic example is the acquisition of Prague-based fintech Twisto, which was first acquired by Zip for €73.8M and subsequently sold to Turkish unicorn Param in a strategic reshuffle. Secondly, Private Equity (PE) is increasingly dominant for scaled platforms. The recent acquisition of Packeta (Zásilkovna) by a consortium of CVC Capital Partners and EMMA Capital highlights PE’s role in rolling up regional winners into international logistics powerhouses. The following section provides an overview of some of the most significant transactions in recent years.

Noteworthy Tech(-enabled) M&A / Exits

5.2 The Buyer Universe: Who is Buying?

Czech tech M&A is fundamentally international. Local corporate buyers are active but tend to focus on smaller, early-stage “capability captures” or talent-driven acqui-hires that rarely make global headlines. The most liquid and high-value exits involve one of two types of international players:

International Strategics: These buyers treat Czech startups as “plug-and-play” growth engines. They buy a finished product and a high-performing engineering team to scale through their existing global distribution channels.

PE & Growth Equity: Financial sponsors have moved from being observers to active “buy-and-build” architects. They focus on tech-enabled infrastructure and logistics assets where they can apply operational upgrades and consolidate fragmented regional markets.

The practical reality for founders is clear: building for an exit requires building for cross-border relevance from day one. Companies with international governance, reporting standards, and customer bases command significantly higher premiums because they appeal to a much wider set of liquid buyers outside the domestic market.

5.3 Consolidation vs. Acqui-hires

The current cycle is defined by fewer, more strategic “platform” bets rather than a high volume of small acqui-hires. Consolidation is the dominant theme in the 2025/2026 market, particularly in the software and IT services sector. While the “Avast-class” outliers remain rare, they provide the necessary credibility to the ecosystem, proving to global LPs that Czech-founded companies can survive the scrutiny of multi-billion dollar strategic consolidations. The defining story of the Czech market is no longer “buying engineers on the cheap,” but rather acquiring “mission-critical capability” with a clear plan for global scaling.