While much of Europe struggles with slow growth, Poland has emerged as one of the region’s quiet outperformers. Over the past three decades, the country has transformed itself from a post-socialist economy into one of the EU’s most resilient growth stories. It leveraged a unique combination of market liberalization, large-scale EU funding, and institutional modernization to build a strong economic foundation – and that foundation now directly supports a rapidly expanding tech and startup ecosystem.

These dynamics position Poland not as an “emerging” ecosystem, but as a maturing CEE powerhouse increasingly competing for international talent and capital.

Riding Europe’s structural tailwinds

Poland’s macro fundamentals reinforce its tech momentum. Sustained GDP growth, one of Europe’s deepest STEM talent pools, and growing integration into global markets have made the country increasingly attractive to founders, investors, and corporates seeking scale within a stable EU jurisdiction.

Several structural forces are accelerating international attention:

Nearshoring and European supply-chain reconfiguration are elevating Poland’s role in tech, cybersecurity, and digital infrastructure

EU digitalisation priorities are channelling funding into R&D, climate tech, and advanced technologies

At the same time, international VCs are looking east for expansion-stage opportunities beyond saturated Western European hubs, while large domestic corporates are stepping up activity in corporate venture, open banking, and digital transformation.

These structural tailwinds flow directly into Poland’s venture market, shaping a VC ecosystem and an M&A landscape that is strong at the early stages, capital-efficient by necessity, and increasingly reliant on international investors as companies scale.

VC Landscape

Poland’s VC and startup ecosystem is shaped by a large pool of technical talent, a strong role for public co-investment, and a clear focus on early-stage B2B and deep-tech companies. Relatively lower operating costs, access to EU funding, and rising participation from foreign VC funds distinguish Poland within the Central and Eastern European (CEE) landscape.

For founders, Poland offers a solid environment to build products and reach early traction. At later stages, however, access to larger growth rounds and experienced senior commercial leadership remains limited domestically. As a result, many companies rely on international investors and cross-border hiring as they scale beyond Series A.

From an investor’s perspective, this structure creates both constraints and opportunities. Limited domestic capital at Series A and growth stages reduces competition for high-quality assets, while valuation levels remain meaningfully below Western European benchmarks. Although regulatory complexity and funding gaps introduce friction, these are generally manageable for investors with experience in cross-border markets.

This dynamic is reflected in the data. As shown in Number of CEE Startups by Country and Stage (Dealroom 2025), Poland leads the region by early-stage startup volume, underscoring the depth of its founder and talent base. However, significantly fewer companies progress to late-stage or €1bn+ outcomes, highlighting a clear scaling gap and the continued importance of international capital at later stages.

Funding by stage

At pre-seed and seed, capital is relatively accessible. Public funding plays a central role: between 2017 and 2023, PFR Ventures invested approximately PLN 1.1bn into VC funds, supporting around 380 startups. This has been reinforced by the FENG programme (European Funds for a Modern Economy), which is deploying roughly PLN 2.1bn into around 40 VC funds, matched by private capital. As a result, pre-seed and seed cheques—typically in the low- to mid-seven-figure PLN range—are widely available, particularly for B2B SaaS, fintech, deep-tech, and AI companies. The main trade-off is slower and more formal investment processes linked to public mandates.

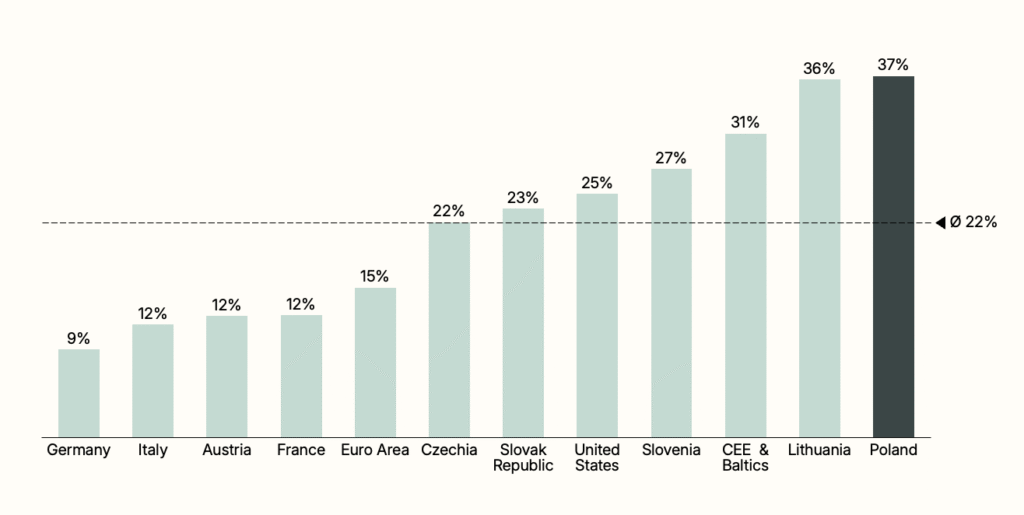

At Series A and beyond, funding becomes more constrained. Only a limited number of domestic funds can lead €5–10m+ rounds, and international investors tend to focus on the top-performing companies. Across CEE, only around 29% of seed-stage startups reach Series A, compared with roughly 48–53% in Western Europe and globally. At the growth stage, most large rounds in Poland are led by foreign funds; in Q1 2025, approximately 42% of total VC investment value came from international investors.

Typical round sizes and valuations

While outcomes vary by sector and traction, some broad patterns apply. Pre-seed rounds commonly range from PLN 0.5–1.5m (€0.1–0.35m), while seed rounds typically fall between PLN 1–5m (€0.25–1.2m), with higher figures for revenue-generating B2B and deep-tech companies. Series A rounds for stronger Polish startups are often in the €5–10m range and are increasingly led by regional or Western European funds.

Valuations generally follow the wider CEE pattern and remain around 30–40% below Western European equivalents. For investors, this translates into more attractive entry pricing and capital-efficient growth; for founders, it raises the bar on traction and international relevance at later stages.

Talent, deal flow, and exits

Talent remains Poland’s strongest structural advantage. The country has one of the largest pools of software engineers and STEM graduates in CEE and leads the region in cumulative startup enterprise value (approximately €58bn). Although wages have risen in recent years, total employment costs remain materially below Western European levels, supporting capital efficiency for scaling teams.

In terms of deal flow, Poland represents the largest and deepest pipeline of tech companies in CEE, accounting for roughly 26% of the region’s total startup enterprise value. Exit outcomes include several high-profile IPOs and acquisitions—such as InPost, Allegro, CD Projekt, and Techland—demonstrating that large outcomes are possible. Outside gaming and e-commerce, however, liquidity remains more limited, and most exits continue to depend on cross-border M&A rather than domestic buyers.

Key considerations for international investors

A significant share of Poland’s VC market is supported by public capital, which has helped deepen early-stage funding but also introduces some dependency on policy continuity and EU funding frameworks. In addition, Poland’s non-euro currency exposes foreign investors to PLN FX risk, alongside inflation-driven cost pressures. While these factors require active management, they are generally familiar and manageable for investors operating across multiple European markets.

M&A Landscape

On the macro side, Poland is one of CEE’s top M&A markets by volume and value. In 2024, it was among the region’s leaders with around €5.8bn of M&A deal value, and remains one of the most active markets in terms of transaction count.

Across CEE, tech remains the most active sector for M&A, with buyers targeting assets that enable digital transformation, AI, and cloud-native services; Poland is one of the volume leaders in that tech dealflow.

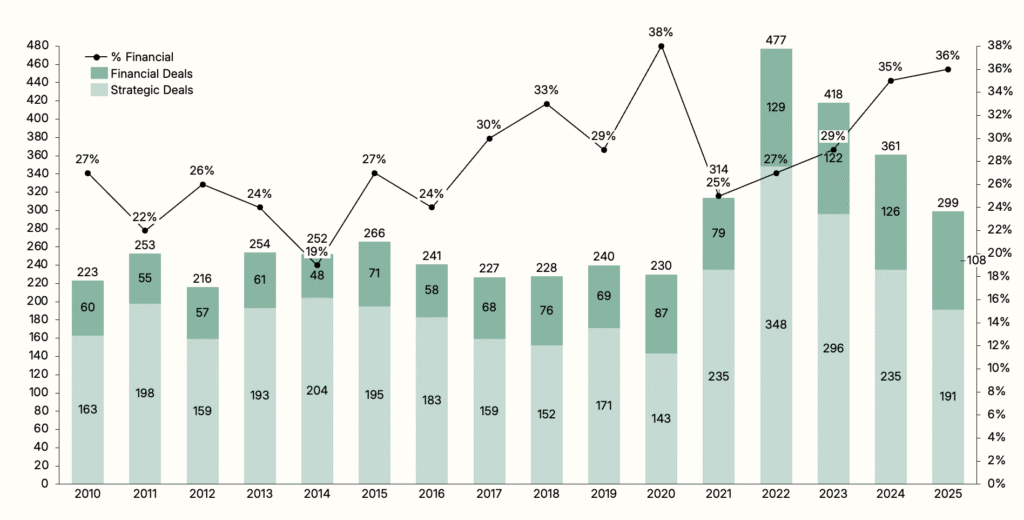

In Poland specifically, software deal volumes have increased ~19x since 2010, and software has recently overtaken industrials as the second-largest sector for M&A by number of deals.

Three structural trends stand out:

Consolidation & roll-ups, especially in software and IT services

PE funds and vertical software consolidators run classic buy-and-build strategies in fragmented markets, using Poland as both a source of targets and a near-shore delivery hub.

Typical targets are profitable SaaS or IT services firms with €2–10m ARR/EBITDA, strong recurring revenue and international client exposure.

Selective large strategic bets

Big, headline deals (InPost IPO, Allegro, Techland, large gaming and e-commerce transactions) show that when a Polish company becomes a category leader, buyers are willing to pay billion-level valuations or list on major exchanges.

Smaller product/team acquisitions and acqui-hires

Below the radar, there is a steady stream of small to mid-size deals where international strategics or consolidators acquire Polish startups for specific capabilities (AI/ML, devtools, cyber, fintech infrastructure) and keep teams in place as local R&D hubs.

Poland offers a mixed exit picture: impressive flagship deals but still a relatively shallow, sector-concentrated market.

On the positive side, the country has produced a string of large, benchmark exits across IPOs and trade sales:

InPost – IPO on Euronext Amsterdam in 2021 at ~$11.6bn valuation.

Allegro – private equity exit followed by a record WSE IPO in 2020, debuting near $19–25bn market value.

CD Projekt, Ten Square Games, Huuuge Games, Grupa Pracuj, Wirtualna Polska – all listed on the Warsaw Stock Exchange, reaching or approaching billion-dollar valuations at or after IPO.

Techland – majority acquisition by Tencent in 2023 at an estimated $1.5bn

Key Innovation Hubs

Poland’s startup activity is concentrated in a handful of major urban hubs, with Warsaw, Kraków, and Wrocław leading the ecosystem. These cities are anchored by strong corporate presence, technical universities, and research institutions, which together drive talent formation and innovation.

Warsaw – fintech, SaaS, and corporate innovation

Warsaw is Poland’s largest technology hub and main financial center. It hosts regional headquarters of global banks and tech companies and is particularly strong in fintech, cloud, cybersecurity, e-commerce, and B2B SaaS.

Both Google and Microsoft operate major engineering centers in the city; Google’s Warsaw hub is its largest engineering center in Europe. Academic anchors such as Warsaw University of Technology and the University of Warsaw provide a large, highly skilled talent pool.

Kraków – engineering, AI, and gaming

Kraków ranks among Poland’s top innovation centers, with strengths in advanced technologies, R&D, and modern business services. It hosts many foreign tech companies and unicorn subsidiaries, with particular depth in software engineering, AI/ML, data, dev tools, and gaming.

Led by AGH University of Science and Technology, local universities supply one of Poland’s largest IT talent pools, making Kraków a popular location for international engineering hubs.

Wrocław – Industry 4.0, robotics, and mobility

Wrocław is a leading technology hub and startup ecosystem, with around 20% of Polish startups registered in the region. Its strong industrial base in automotive, electronics, and machinery underpins a growing focus on Industry 4.0, automation, and robotics.

The combination of industrial corporates, R&D, and engineering talent makes Wrocław a natural cluster for industrial tech, mobility, and hardware–software innovation, supported by Wrocław University of Science and Technology.

Outlook

Next Generation of Winners

Gaming is undervalued as an innovation engine. CD Projekt, Techland, Bloober Team, and People Can Fly have established Poland as one of the world’s top five gaming nations by output quality. The next wave is the tooling, engine infrastructure, and AI-assisted development pipelines being built by veterans leaving these studios — and Warsaw and Kraków are already seeing the first spin-outs.

Logistics and supply chain software has a natural home in Poland. The country is the EU’s largest road freight market, sitting at the intersection of East-West and North-South trade corridors. InPost succeeded because of Poland’s geography, not despite it. The next generation of winners in last-mile, warehouse automation, and cross-border trade infrastructure will likely emerge for the same structural reason.

Defence and dual-use tech is a category that would have seemed niche three years ago. Poland now spends over 4% of GDP on defence — the highest in NATO — creating a domestic procurement pipeline that simply doesn’t exist in most European ecosystems.

VC Market Evolution (2025–2027)

The FENG programme’s PLN 2.1bn deployment keeps seed and early Series A well-capitalised through at least 2027. The constraint remains Series B and beyond, where domestic capital has always been structurally absent.

The more consequential dynamic is what happens to the first generation of PFR-backed funds now returning capital. A handful will raise successor funds with meaningful private LP participation — this moment determines whether Poland builds a genuine domestic VC institutional layer or remains dependent on public co-investment.

M&A Outlook

Industrial and logistics software is the most likely volume driver. Poland’s manufacturing base — automotive in Wrocław and Silesia, electronics, aerospace — is digitising, and the software serving it is fragmented and founder-owned. Classic PE consolidation territory.

Gaming M&A will continue. The Tencent-Techland deal at ~$1.5bn confirmed that Polish studios carry real international strategic value. Mid-tier studios with strong IP remain credible targets for Asian and US buyers.

Warsaw’s financial sector will drive fintech acqui-hires. PKO BP, Pekao, and mBank are all running digital transformation programmes where acquiring beats building — particularly in payment infrastructure and open banking.

Long-Term Positioning

Poland’s credible long-term claim is as the engineering backbone of European software infrastructure — less visible than London or Berlin at the product layer, but deeply embedded in what those products run on.

The single most important variable is whether the gaming generation converts its experience into a founding wave the way Skype alumni did in the Baltics. Early signs suggest it already is.