1. Economic Trends and the Shift Toward Innovation

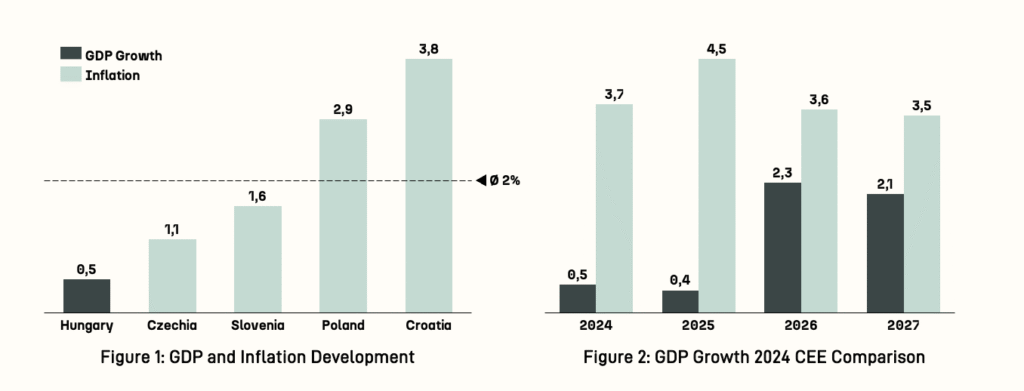

Hungary’s economy has been slow to recover after a difficult couple of years. Growth in 2025 was limited, and while things are expected to improve in 2026 and 2027, inflation is still high (Figure 1).

The contrast with neighbouring countries is clear. Poland and Croatia are both growing at over 3%, while Hungary is lagging behind (Figure 2). Most of the growth that does exist is coming from consumer spending, helped along by higher wages and planned tax cuts. Business investment is a different story: it has dropped nearly 20% since early 2023 and is not expected to recover until 2027.

On the industrial side, Hungary has made a big bet on electric vehicles and batteries. Weak demand from Germany and the rest of the Eurozone has kept production below capacity for now, but this is still central to Hungary’s export plans as new facilities come online.

Business and Industrial Services was the most active sector for deals in the first half of 2025. Together with growth in Agriculture Tech and consumer electronics, this points to an economy that is gradually changing shape.

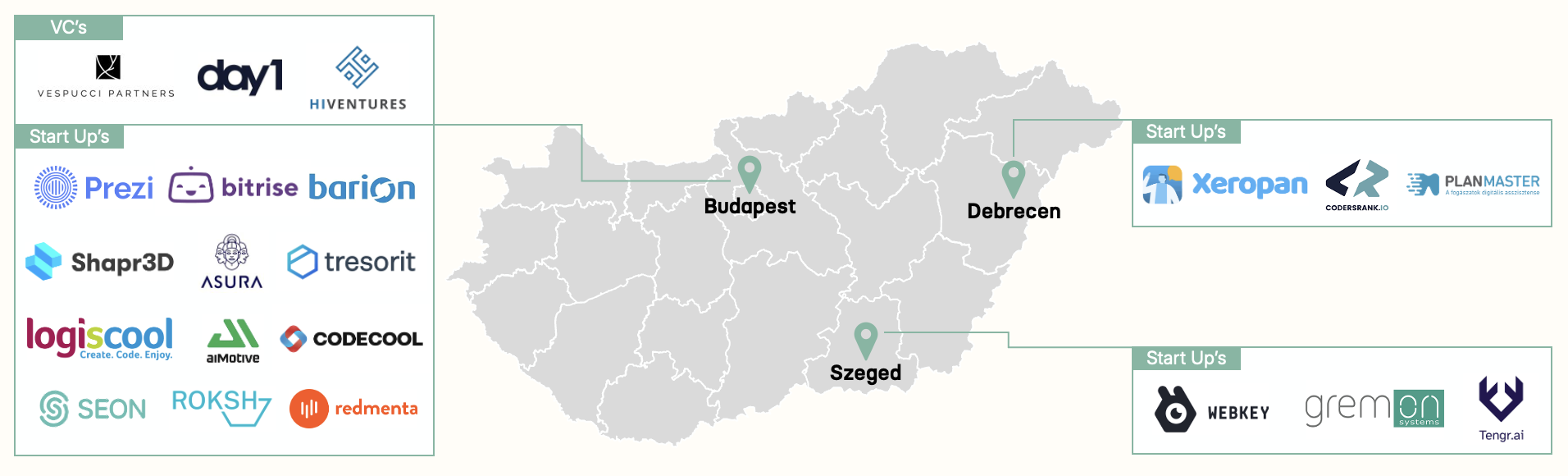

This shift is also showing up in the startup world. As traditional industries face pressure, founders are moving toward high-tech B2B products. Today, 36% of Hungarian startups are focused on artificial intelligence. That number tells you something about where things are headed.

Hungary also has a small number of high-profile startup events, and most of them take place in Budapest. This reinforces how centralised the ecosystem is.

Hungary also has a small number of high-profile startup events, and most of them take place in Budapest. This reinforces how centralised the ecosystem is.

- Budapest Startup Safari opens Budapest’s startup and VC offices to international visitors.

- Brain Bar Budapest is a large tech and ideas event that attracts an international audience.

- Startup Weekend Budapest and Startup Grind Budapest keep the local community active throughout the year.

3. Funding

3.1 Where the Money Went

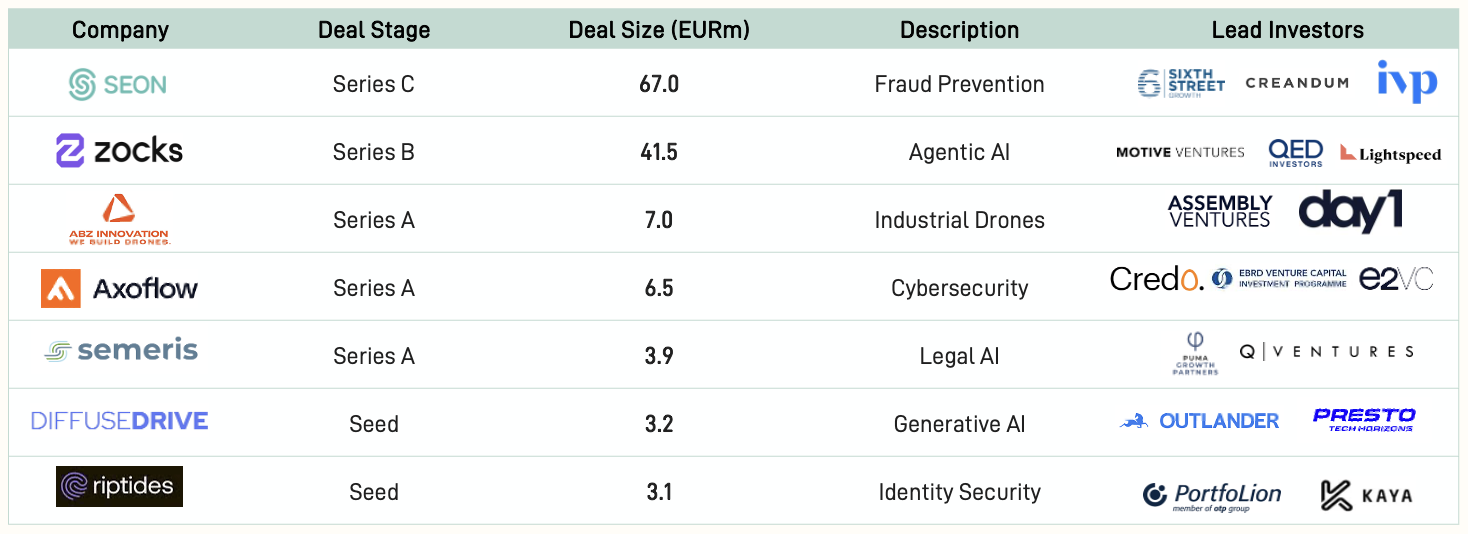

In 2025, investors focused on a narrow group of Hungarian startups: those building tools for businesses, particularly in security, compliance, AI, and software infrastructure. Consumer apps were not the priority. Investors wanted specialized products with paying customers outside Hungary.

The companies that raised the most money follow a similar pattern: strong Hungarian engineering teams, but built and funded with international markets in mind. Axoflow and Riptides in cybersecurity. Zocks and DiffuseDrive in AI. These are the companies that represent Hungarian tech to the rest of the world.

3.2 Key Trends

The numbers from the first half of 2025 tell an interesting story. The number of deals rose by 17.5%, but the total amount raised fell by 45.7% compared to the same period the year before. More rounds, but smaller ones on average.

The money that was raised stayed concentrated in a few areas: Business and Industrial Services, consumer electronics, and specialist software. Venture capital accounted for around 72% of deals by number, but growth-stage private equity absorbed more than three quarters of the total capital. Early-stage activity was busy. The big money, however, went to later-stage companies.

The most significant change is in where the capital is coming from. In 2025, a much higher share of rounds included foreign investors compared to 2024, particularly in cybersecurity, AI, and enterprise software. The pattern is now well established: Hungarian teams building for global markets, backed by international investors.

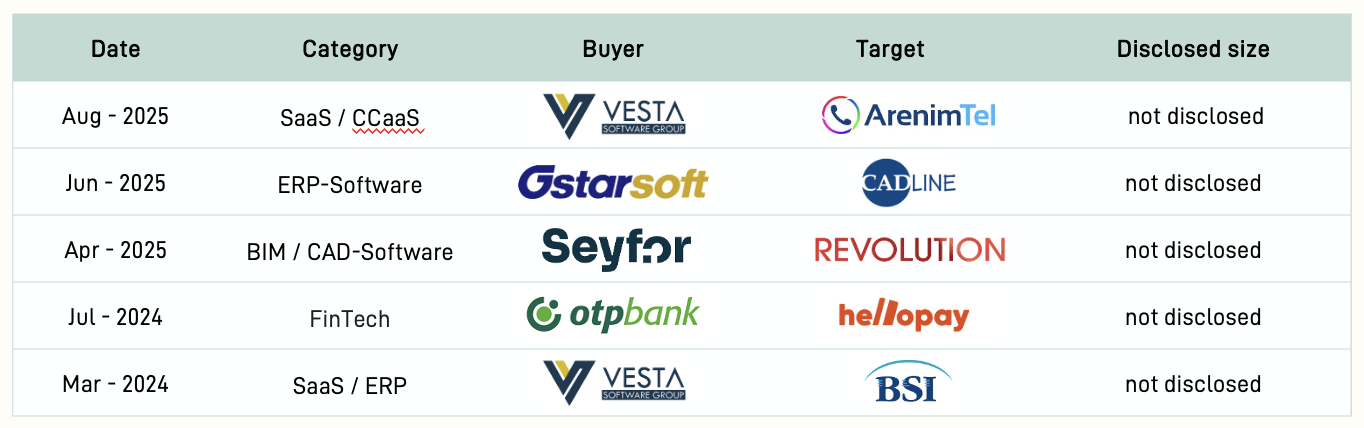

4. M&A in Hungary

4.1 Software Leading the Way

Tech M&A in Hungary is concentrated in software: SaaS, ERP, financial technology, and customer communication platforms. Most deals are mid-sized, and nearly all are private transactions with no public price tag.

The same buyers keep appearing. Vesta Software Group shows up multiple times, running a deliberate acquisition strategy. Seyfor and Gstarsoft are also active. These are not opportunistic deals. These buyers are carefully expanding their portfolios, one targeted acquisition at a time.

The overall picture is of Hungary as a reliable source of specialized software companies within Central and Eastern Europe. There are no blockbuster deals here. Instead, the market is built on frequent, careful acquisitions of profitable niche businesses with solid customer bases and steady revenue.

It is a market that is maturing but still quite fragmented. Value comes from deep product knowledge, focus on specific industries, and thoughtful integration rather than size alone.